✨ AI Summary

- Title: Revolutionizing Home Loans: The Rise of DeFi Lending Platforms

In a world where traditional home loan processes create barriers for borrowers like Sarah and Raj, DeFi lending platforms powered by blockchain technology offer a promising solution.

- By eliminating intermediaries, increasing transparency, and automating approvals through smart contracts, DeFi home loans bring faster approvals, lower fees, and inclusivity for gig workers and the unbanked.

- Tokenizing real estate and utilizing stablecoins as collateral redefine ownership and streamline the lending process.

- While challenges such as regulatory uncertainty and security risks exist, solutions like regulatory compliance frameworks and third-party audits mitigate these concerns.

- The future of homeownership is borderless, bias-free, and accessible to all, ushering in a new era of DeFi-powered home loans.

- A Tale of Two Borrowers

- Caveats of Traditional Home Loan Processing

- Enter Blockchain-Based Home Loan Disbursement or DeFi Home Loans

- Building the DeFi Home Loan Platforms: How It Could Work

- Benefits of DeFi Home Loans Over Traditional Home Loans

- Challenges & Solutions in DeFi Home Loan Platform Development

- A New Era of Homeownership Powered By Blockchain

A Tale of Two Borrowers

Imagine two homebuyers:

- Sarah, a freelance designer with a stellar rental history but no traditional credit score, waits 42 days for a bank to reject her mortgage application.

- Raj, a tech worker in Lagos, pays 15% extra in hidden fees to navigate cross-border loan bureaucracy.

Meanwhile, in a decentralized world, an AI-powered DeFi lending platform offering home loans accesses Sarah’s crypto holdings and gig income, approving her loan in 8 minutes. Raj collateralizes his tokenized land in seconds, bypassing banks entirely. This isn’t a distant dream. Dubai recently launched the Real Estate Tokenization Project, setting a standard with tokenized lands. Given its potential and regulatory support, as Trump crushes the IRS rule, DeFi lending platform development will dominate the home loan sector.

Caveats of Traditional Home Loan Processing

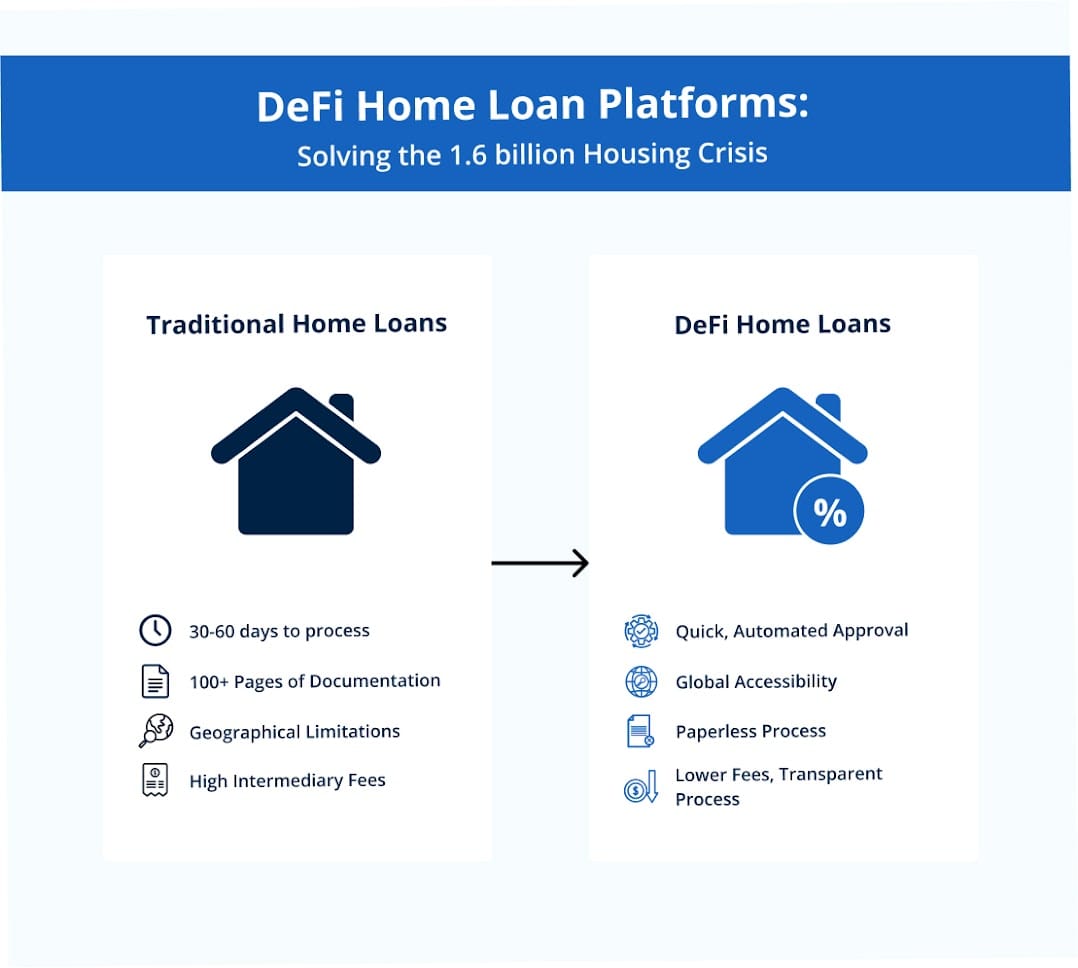

For generations, the path to homeownership has involved navigating the intricate, often cumbersome, process of securing a traditional mortgage. Much like an old, complex lock mechanism requiring numerous keys held by different parties, this process, although ubiquitous, has served its purpose yet is frequently characterized by delays, high costs, and a lack of transparency. It’s a system built on intermediaries and paper trails, often leaving borrowers overwhelmed and underserved, creating a compelling case for exploring alternative models like dedicated DeFi lending platform development.

- Average Approval Time: It takes 45-60 days on average to close on a house when financing is involved, whereas cash purchases take as little as 7-10 days. While fintech innovations, such as online applications and automated underwriting, have reportedly shaved about a week off processing times, the overall duration remains a significant hurdle and source of anxiety for buyers.

- Rejection Rates: Gaining mortgage approval is not guaranteed, and significant disparities based on race, demographic groups, interest rates, and ethnicity may exist. More than half of Americans, as per a survey by Bankrate, applied for a loan or financial product, and 48% of those faced rejections on at least one application. Home Mortgage Disclosure Act (HMDA) data reveals denial rates for conventional home loans in 2023: 16.6% for Black applicants and 12.0% for Hispanic-White applicants, compared to 9.0% for Asian applicants and 5.8% for non-Hispanic White applicants.

- Hidden Costs: Beyond the hefty down payments, borrowers face a barrage of closing costs, including transfer taxes, appraisals, inspections, title searches, insurance, fees for attorneys, loan origination, underwriting, credit checks, etc. As per Bankrate’s survey, these costs may round off to $7500, adding thousands of dollars to the transaction. This cost burden directly impacts housing affordability, making it even harder for first-time homebuyers to own a necessity. These rising costs quickly erode home equity before it even begins to build, strengthening the argument for exploring systems like DeFi home loans that promise lower transactional overhead.

- Opacity and Global Exclusion: The traditional mortgage process is notoriously complex, involving a multitude of intermediaries—lenders, brokers, appraisers, title companies, insurers, and government agencies. This complexity often translates into excessive paperwork and a lack of transparency for the borrower, making consumers feel more confused, intimidated and misled about terms and costs. Moreover, as per the World Bank, more than 1.7 billion adults are unbanked, locked out of the mortgage markets, demonstrating a huge potential for DeFi lending platform development that offers global accessibility.

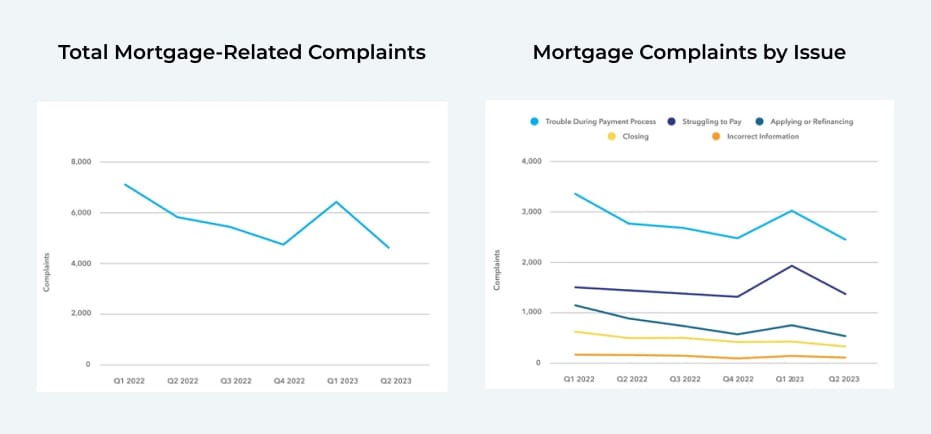

Source: CFPB

- Borrower Frustrations: Compiling these issues leads to widespread borrower frustration, documented through surveys and consumer complaints. The CFPB received a significant number of mortgage-related complaints in 2022-2023, with the largest categories being trouble during the payment process, issues with loss mitigation, problems applying for or refinancing a mortgage, etc. Homebuyers also reported frustration with cited document errors, lengthy in-person appointments, unexpected travel or caretaking costs, etc.

In brief, here’s why traditional home loan systems need a rethink:

- Manual Processes: Paperwork, profuse verification steps, prolonged waiting periods, credit checks, and underwriters slow everything down.

- Opaque Fees: Banks profit from complex fee structures.

- Bias: Human underwriters (consciously or not) favor high-income, traditional applicants.

- Border Barriers: Currency conversions, international regulations, and lack of collateral options.

Enter Blockchain-Based Home Loan Disbursement or DeFi Home Loans

A potentially more disruptive force is emerging, built on the foundation of blockchain technology. But the question remains: could DeFi open the door differently, offering a better alternative to conventional home loans? Let’s explore:

Home Loan DeFi lending platform development replaces banks with code, collateral with crypto, and bias with AI. Here’s how:

- Smart Contracts: The Invisible Loan Officer

- Automated Approvals: Loan terms are pre-coded into smart contracts. If Sarah’s crypto wallet and rental NFT meet criteria, the loan executes instantly.

- Transparent Fees: Every cost is visible on-chain. No surprises. Plus, no intermediaries, so no scope of hidden costs.

- AI-Powered Underwriting

- Alternative Data: Analyzes crypto holdings, rental NFTs, or even social media cash flows.

- Bias-Free Scoring: Algorithms ignore race, gender, or zip code.

- Borderless Collateral

- Tokenize real estate, use stablecoins, or stake crypto assets to secure loans—no borders, no banks.

Building the DeFi Home Loan Platforms: How It Could Work

Leveraging the capabilities of blockchain, smart contracts, and AI, a DeFi home loan platform could automate and streamline many aspects of the traditional lending process, creating a potentially more efficient and transparent system

Conceptual Framework: The core idea involves replacing manual processes and intermediary functions with automated logic executed by smart contracts. Borrowers and lenders (or liquidity providers) would interact directly with the protocol, often through a web-based dApp.

Potential Process Flow:

- Origination/Application: A prospective borrower initiates the process via the dedicated DeFi lending platform DApp. Application data, including identity verification, could be submitted digitally. This might involve integrating with decentralized identity solutions or utilizing specialized oracles to perform KYC/AML checks in a way that balances privacy with regulatory compliance.

- Underwriting Automation: Smart contracts integrated within DeFi lending platform development would execute predefined underwriting rules based on the submitted data. This automated assessment could involve verifying identity, analyzing income and assets (potentially through oracles connecting to traditional data sources or analyzing the borrower’s on-chain financial history), and evaluating creditworthiness. While some envision using alternative data for credit assessment, current mortgage regulations often mandate traditional credit checks, posing a challenge for purely DeFi models.

- The Role of Tokenized Real Estate: A key concept enabling DeFi mortgages is the tokenization of real estate. This involves converting the ownership rights of a physical property into digital tokens recorded on a blockchain (perhaps NFTs). Potential benefits of home loan DeFi lending platform development include enabling fractional ownership, increasing liquidity, enhancing transparency of ownership records, and broadening access to real estate investments. In a DeFi home loan scenario, a token representing the property could be locked within a smart contract as collateral securing the loan.

- Loan Disbursement: Once underwriting conditions are met and collateral is secured, the smart contract could automatically release the DeFi loan funds to the borrower. These funds would likely be in the form of stablecoins (cryptocurrencies pegged to fiat currencies like the US dollar) to minimize volatility during the transaction.

- Repayment & Servicing: Smart contracts would manage the entire loan lifecycle, including the repayment schedule. Payments, likely made in stablecoins, would be automatically collected and recorded on the blockchain. Interest rates could be fixed or variable, potentially determined algorithmically based on the supply and demand within the platform’s liquidity pools, similar to established DeFi lending protocols like Aave and Compound. Alternate interest rate mechanisms can be set up during DeFi lending platform development. The DeFi loan status, payment history, and outstanding balance would be transparently available on the blockchain.

- Liquidation: In the event of default or if the value of the collateral (as reported by a price oracle) falls below a predetermined threshold (e.g., a specific loan-to-value ratio), the smart contract could automatically trigger a liquidation process. This would involve selling the locked collateral (the property token) on a decentralized exchange or auction platform to recover the outstanding loan amount, mirroring liquidation mechanisms in existing DeFi lending protocols.

Benefits of DeFi Home Loans Over Traditional Home Loans

Benefits of Home Loan DeFi Lending Platforms for Borrowers:

- Potentially lower interest rates: 50-70% lower fees and thousands of dollars saved by eliminating intermediaries.

- Faster loan approval processes: Facilitating approvals in hours and not weeks or months.

- More flexible loan terms: DeFi home loans give power back to people.

- Inclusivity: DeFi lending platform development solutions serve gig workers, global citizens, and the unbanked.

- Transparency: Every fee and term is on-chain and therefore traceable.

Benefits for Lenders:

- Opportunity for higher returns compared to traditional savings accounts.

- Greater control over their investments.

- Transparency in loan origination and repayment.

Challenges & Solutions in DeFi Home Loan Platform Development

- Regulatory Uncertainty

- Challenge: Governments are still defining legal status. DeFi lending platform development for home loans may involve collaborating with professional legal attorneys.

- Solution: Work with regulators to build compliant frameworks (e.g., KYC/AML integrations, DID solutions).

- Crypto Volatility

- Challenge: A Bitcoin crash could trigger mass loan liquidations.

- Solution: Use overcollateralization (e.g., 150% collateral ratios) and stablecoin pegs.

- Adoption Hurdles

- Challenge: Mainstream users fear blockchain complexity.

- Solution: Simplify UX—think “one-click” DeFi wallets and AI-guided interfaces.

- Security Risks

- Challenge: Smart contract bugs could expose funds to huge risks, making DeFi home loans riskier.

- Solution: Third-party audits (e.g., CertiK) and insurance pools.

For more challenges and solutions, you can schedule a call with subject matter experts and they’ll address your DeFi lending platform development concerns.

A New Era of Homeownership Powered By Blockchain

DeFi home lending isn’t just about technology but about redefining access. The question isn’t if DeFi will disrupt home loans—it’s how fast. As Sarah and Raj unlock homes once out of reach, the old system’s walls crumble. The blueprint is clear: Home Loan DeFi Lending Platform Development is building a world where ownership is borderless, bias-free, and belongs to everyone.

“In the future, your home loan officer might just be a few lines of code—and that’s a good thing.”

Ready to explore DeFi home lending?

Antier is proud to be at the forefront of this transformation. Our expertise in DeFi protocol engineering, real estate tokenization, and compliant lending dApp development positions us as a strategic partner for businesses ready to disrupt the conventional home loan landscape.

Let’s collaborate to change the rules.