✨ AI Summary

- Discover how Singapore banks can overcome regulatory, operational, and strategic challenges by implementing MAS-compliant white-label crypto wallets.

- These wallets offer pre-architected solutions that address regulatory uncertainty, legacy infrastructure gaps, and customer-centric needs.

- By partnering with a trusted provider like Antier, banks can launch compliant wallets in just 2 weeks, ensuring regulatory alignment and faster market entry.

- Learn from a Tier-1 bank case study that achieved 6x ROI in 60 days by offering digital asset services through a white-label crypto wallet.

- With features like on/off ramps, co-branded crypto cards, and AI agents, these wallets enable seamless integration and enhanced security.

- Understanding The Pain Points of The Singapore Banks

- Why Singapore Banks Need an MAS-Compliant White-Label Crypto Wallet Platform Immediately?

- Antier’s Capabilities: MAS-Compliant White Label Crypto Wallet Development

- Case Study: How A Tier-1 Bank Achieved 6x ROI in 60 Days With a White-Label Crypto Wallet?

- Launch Your MAS-Compliant White Label Crypto Wallet in Just 2 Weeks!

- Roll Out a MAS-Compliant White Label Crypto Wallet Now!

Are Singapore banks truly prepared to shape the future of Web3 finance? Institutions that integrate MAS-compliant white-label crypto wallets gain a strategic advantage in an era when decentralized protocols and tokenized assets are redefining value exchange. Banks can become active architects of programmable finance by embedding regulated on-chain infrastructure—governing liquidity pools, securing digital custody, and establishing trust anchors within decentralized ecosystems. This transformative capability positions forward-looking banks at the vanguard of Singapore’s Web3 evolution, enabling them to influence interoperability standards and drive institutional adoption of blockchain-native services.

Understanding The Pain Points of The Singapore Banks

As Singapore intensifies its role as a regional hub for digital assets, the Monetary Authority of Singapore (MAS) has implemented some of the most comprehensive crypto regulations in the world. For banks looking to integrate digital assets, the following challenges dominate the landscape:

Challenge 1. Regulatory and Compliance Complexity

- Licensing Requirements : Under the Payment Services Act (PSA), banks offering digital payment token (DPT) services must be licensed and adhere to strict compliance requirements, including KYC (Know Your Customer), CDD (Customer Due Diligence), and ongoing monitoring obligations.

- Travel Rule Compliance : MAS mandates full adherence to the FATF Travel Rule, requiring banks to collect, verify, and transmit originator and beneficiary information for crypto transactions.

- Custody and Asset Safeguarding : Banks are required to keep approximately 90% of digital assets in cold storage with multi-signature configurations, segregate client assets, and enforce trust account structures.

Challenge 2. Operational and Technological Limitations

- Legacy Infrastructure Gaps : Traditional banking systems were not designed for blockchain or crypto-native operations. Integrating wallets, custody solutions, and trading infrastructure creates major complexity.

- Security and Risk Exposure : Banks face heightened risks from hacking, asset theft, and compliance breaches due to unfamiliarity with decentralized architectures and digital asset custody requirements.

- Inadequate AML Controls : Manual or legacy AML tools are insufficient for monitoring high-frequency crypto transactions. This leads to delayed onboarding, high false positives, and regulatory non-compliance.

Challenge 3. Strategic and Market Pressures

- Time-to-Market Risks : Internal development of compliant crypto infrastructure can take 12–18 months or more, delaying market entry and increasing sunk costs.

- Customer Attrition to Fintechs : Agile fintech players already offer seamless crypto experiences, including DeFi access, staking, and 24/7 OTC trading. Banks risk losing HNW and institutional clients if they cannot match these offerings.

- Reputational and Regulatory Exposure : Failure to launch compliant services or meet MAS audit requirements could result in penalties and reputational harm, making it crucial to adopt reliable and vetted platforms. Let us now begin to understand how these challenges of the banks in Singapore can be addressed by white-label crypto wallets.

Why Singapore Banks Need an MAS-Compliant White-Label Crypto Wallet Platform Immediately?

1. Regulatory Uncertainty & Compliance Risk – These crypto wallet platforms are pre-architected to satisfy MAS regulatory requirements under the Payment Services Act, including trust account management, KYC/AML, and transaction monitoring, minimizing institutional exposure to legal risk.

2. Siloed Legacy Infrastructure – API-first white-label crypto wallet stack integrates directly with banks’ core systems, enabling seamless orchestration of fiat, crypto, and compliance services across front- and back-office infrastructure.

3. Lack of Crypto-Ready Payment Channels – With in-built on/off ramps and co-branded card issuance, these wallets unlock instant crypto-to-fiat interoperability, turning a regulatory bottleneck into a monetized channel.

4. Customer-Centric Experience – The white-label crypto wallet development solution supports mobile, desktop, and super-app environments, allowing banks to deliver a crypto-native UX inside their digital ecosystem without fragmenting customer journeys.

5. High Compliance Overhead for AML/KYC – Automated ID verification, AI-driven risk scoring, and continuous transaction screening significantly reduce the manual workload of compliance teams, while satisfying MAS obligations.

6. Crypto Asset Security and Custody – Built-in institutional-grade custody (cold storage, multi-sig, and hardware wallet compatibility) ensures safe digital asset management that adheres to MAS’s 90% offline storage directive.

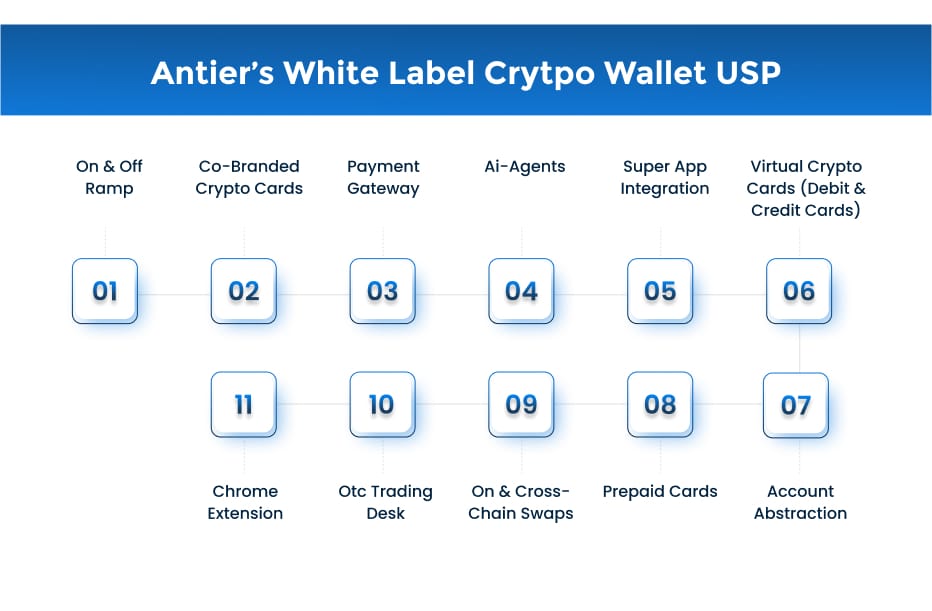

Antier’s Capabilities: MAS-Compliant White Label Crypto Wallet Development

Antier offers a fully white-label, MAS-aligned white-label crypto wallet platform engineered for global banks and compliance-driven institutions. Banks should evaluate crypto wallet platforms based on institutional-grade features and MAS compliance. Here is what makes Antier, the most trusted and experienced white label crypto wallet development company-

✓ On & Off Ramp : We provide seamless fiat-to-crypto and crypto-to-fiat conversion right inside the wallet, enabling regulated entry and exit points. This onboarding/offboarding capability automates KYC/AML checks and trust-account handling, so customers can easily buy or sell crypto via bank transfers or cards. It bridges traditional finance and digital assets in one interface. For banks, it ensures adherence to MAS fiat custody rules and a smooth user journey into DeFi.

✓ Co-Branded Crypto Cards : Enables financial institutions to issue Visa/Mastercard-style co-branded crypto cards with the bank’s identity, backed by customers’ crypto balances. These cards let users spend crypto at any merchant, instantly converting to fiat at the point of sale. All transactions flow through the bank’s AML/KYC processes and audit logs, assuring regulators that card spending is fully transparent and compliant.

✓ Payment Gateway : Acts as an embedded, regulated crypto payment processor within the white-label crypto wallet app. Merchants and users can send or accept cryptocurrency for goods and services, with backend conversion into local currency. This gateway supports borderless commerce with transparent settlement and lower fees. Crucially, every payment is monitored by built-in compliance rules and transaction reporting. Institutions gain a turnkey crypto checkout solution that aligns with MAS regulations, boosting revenue while safeguarding against fraud and money laundering.

✓ AI Agents : Integrates smart, AI-driven assistants to automate and personalize user interactions. Examples include voice or chatbots that guide customers through transfers, portfolio rebalancing bots that suggest trades, and monitoring agents that flag suspicious activity in real time. These agents provide 24/7 customer support and proactive fraud/AML alerts, reducing manual overhead.

✓ Super App Integration : Designed for plug-and-play embedding into existing banking or financial “super-apps.” The white-label crypto wallet can be launched as a new tab or module in a mobile banking app, giving customers unified access to crypto alongside traditional services. This integration preserves the host app’s security posture and compliance flows (SSO, MFA, KYC).

✓ Virtual Crypto Cards : Offers instant issuance of digital (stablecoin-backed) debit or credit cards for crypto spending. Each virtual card is linked to the crypto wallet and automatically converts crypto to fiat at purchase time. Users can pay online or in-app with these cards just like any credit/debit card, eliminating volatility risk. From a compliance perspective, every card transaction is subject to AML checks and spending limits under the bank’s program.

✓ Account Abstraction : Implements advanced wallet logic that decouples user identities from raw blockchain accounts. This enables user-friendly features such as gasless transactions (the platform pays fees), batched or scheduled payments, and simpler key recovery. It reduces transaction costs and security risks by abstracting on-chain complexity (for example, using social recovery instead of private key loss). Importantly for institutions, every abstracted transaction is still logged and auditable. The abstraction layer preserves transparency while enabling a smoother user experience aligned with enterprise security standards.

✓ Prepaid Cards : Prepaid cards when integrated into white label crypto wallet apps allows institutions to issue crypto-backed prepaid cards that customers can top up, reload, and spend like traditional prepaid cards. These cards bridge the crypto and fiat worlds: users load crypto, then spend dollars/pesos/etc. via the card. The system can include rewards or loyalty programs. Built-in compliance measures enforce spending limits, KYC for each cardholder, and real-time tracking of card activity. This feature essentially delivers crypto utility (easy spending) under the same regulatory framework as fiat payment cards, satisfying audit and regulatory requirements.

✓ On & Cross-Chain Swaps : Features an integrated swap engine for instant token exchange both within the same blockchain and across different chains. Users can, for example, swap Ethereum tokens or move assets between Ethereum and a separate blockchain without leaving the wallet. This increases liquidity and convenience. Technically, swaps use smart routing or AMMs under the hood.

✓ OTC Trading Desk : Facilitates high-volume, off-exchange crypto trades for institutions seeking deep liquidity without slippage. The integrated OTC desk enables banks and regulated entities to execute large trades directly with verified counterparties, backed by custody and escrow mechanisms. With real-time settlement, fixed pricing, and built-in compliance controls (KYC/AML screening, reporting), it ensures confidential, efficient, and fully MAS-compliant bulk trading execution.

✓ Chrome Extension : Provides a secure browser extension for easy Web3 access. Users can manage assets, sign transactions, and interact with dApps directly from their browser. This is especially useful for power users and businesses needing quick access. The extension enforces multi-factor authentication and encryption for key operations.

Each of these capabilities addresses banks’ key requirements for security, compliance, and client demand. Together, they ensure a crypto wallet development solution is not just feature-rich but fully aligned with MAS regulations, giving senior managers confidence to expand into digital assets. Thus, it is necessary that Singapore banks adopt white label crypto wallet development solutions for faster market entry and offer their end users with enhanced digital custody.

Case Study: How A Tier-1 Bank Achieved 6x ROI in 60 Days With a White-Label Crypto Wallet?

“Success breeds confidence, and proven results underpin trust. Reading success stories before investment allows stakeholders to assess viability and mitigate risk.”

A Singapore-based top tier-1 bank aimed to offer digital asset services to its HNW and corporate clients without building in-house infrastructure.

- Key Challenges

The bank faced an urgent requirement to offer an MAS-compliant white-label crypto wallet platform, as clients increasingly sought access to regulated crypto services within a trusted banking environment. However, the internal roadmap for crypto wallet development spanned over six months and required extensive compliance vetting, infrastructure investment, and custom integrations. Meanwhile, premium clients were already beginning to shift their digital asset exposure to offshore platforms offering faster onboarding and higher asset flexibility, jeopardizing both client retention and wallet share.

- The Solution

Partnered with a top white-label crypto wallet service provider to launch a fully MAS-compliant, branded crypto wallet — integrated with SGD rails, custody layers, and real-time KYC/AML monitoring — in just 7 days.

- Strategic Outcome

- First-mover advantage among domestic banks.

- Secured strong client retention by offering digital asset services under one roof.

- Launched in under 2 weeks with zero regulatory roadblocks

- 6X ROI in 60 days through transaction fees and client engagement

- 1000s of new digital asset users, with minimal CAC

This case study underscores how adopting a MAS-compliant white-label crypto wallet development solution enabled the bank to meet client demand, achieve ROI, and fortify its market position. Stakeholders seeking to replicate this success should partner with trusted and the best white-label crypto wallet service providers to ensure regulatory alignment and excellence.

Launch Your MAS-Compliant White Label Crypto Wallet in Just 2 Weeks!

A globally recognized white-label crypto wallet development company leverages modular infrastructure and deep compliance expertise to deliver MAS-compliant crypto wallets for banks and fintech institutions in record time. Here’s how such a wallet is deployed—strategically and securely—within just 14 days:

- Day 1 : Strategic Alignment & Regulatory Planning

Initial alignment between the bank’s legal, compliance, and tech teams and the crypto wallet development partner. Key goals include defining wallet architecture, identifying mandatory MAS compliance layers (KYC, AML, PSA licensing), and planning trust account structures and custody models. This creates the legal and technical baseline.

- Day 2–3 : Infrastructure Configuration & Security Architecture

Cloud or on-prem infrastructure is provisioned with secure elements—cold storage, multi-signature wallets, encrypted key vaults, and internal firewalls. Regulatory audit logs and institutional-grade network security protocols are deployed. This lays the technical foundation for MAS-compliant crypto wallet operation.

- Day 4–6 : Custom Feature Integration & System Interoperability

The white-label crypto wallet platform is customized with feature modules like on/off-ramp rails, OTC trading, AI agents, virtual crypto cards, and embedded compliance workflows. APIs are integrated with FAST/PayNow systems, payment gateways, and the bank’s internal platforms to ensure ecosystem interoperability.

- Day 7–8 : KYC/AML Embedding & Compliance Automation

MAS-aligned KYC/AML flows are enabled through integration with licensed verification providers or internal systems. This includes identity verification, transaction monitoring, and rule-based flagging. Fiat movements are routed via authorized payment institutions into regulated trust accounts with real-time traceability.

- Day 9–10 : Institutional Testing & Security Validation

All wallet functionalities—from onboarding to swaps, OTC execution, and withdrawals—are tested under simulated high-load environments. Penetration testing and compliance checks are completed to ensure encryption, data privacy, transaction auditing, and smart contract layers meet MAS thresholds.

- Day 11–12 : Training & Pilot Rollout

Internal teams are trained on compliance protocols, wallet usage, and customer issue management. A pilot rollout is launched in a controlled sandbox or with a limited user group to test production-readiness. This feedback loop is used to fine-tune operational readiness.

- Day 13–14 : Full Launch & Post-Launch Monitoring

The white-label crypto wallet is launched institution-wide. Real-time monitoring of transactions, user activity, compliance alerts, and system performance is activated. The development partner offers SLA-based support, performance tuning, and periodic MAS compliance updates, ensuring continuous operational integrity.

Are you planning to offer the best digital asset management and custody experiences to the end users in Singapore? If yes, then this is high time you must hire the industry’s most experienced team of certified blockchain professionals who offer comprehensive white-label cryptocurrency wallet development services.

Roll Out a MAS-Compliant White Label Crypto Wallet Now!

Antier’s MAS-ready white-label crypto wallet solution aligns seamlessly with Singapore’s Payment Services Act and emerging digital-asset regulations.

- Rapid Deployment in 14 Days : Pre-configured modules ensure PSA compliance, automated KYC/AML, and robust liquidity aggregation, reducing time-to-market from months to weeks.

- Enterprise-Grade Security : Military-grade encryption, DDoS mitigation, and optional decentralized identity protocols protect assets and data.

- Ongoing Compliance Support : 24/7 technical assistance and proactive regulatory updates guarantee sustained MAS alignment.

- Cost Efficiency: White-label deployment slashes development and maintenance expenses by up to 70% compared to in-house alternatives.

Accelerate your digital-asset strategy—secure market leadership and cost advantage with the industry’s top crypto wallet development company’s MAS-compliant wallet solution.