✨ AI Summary

- In the evolving landscape of global banking, RWA Tokenization is reshaping how financial institutions manage assets, risk, and investment opportunities.

- This technology transforms traditional assets into programmable tokens, streamlining lending operations, enhancing capital markets, optimizing cross-border payments, enabling custody and asset management, and ensuring regulatory compliance.

- The RWA Tokenization Lifecycle involves asset identification, token design, generation, ledger mapping, deployment, trading, and renewal.

- Investment banks are leveraging tokenization for programmatic trading, portfolio management, and data governance.

- Major banks like JPMorgan and Goldman Sachs have already integrated tokenization into their platforms.

The Global Banking Institutions are adapting Tokenization Development services to deliver efficient, secure, and customer-centric financial services. These platforms are redefining how banks handle assets, risk, and investment opportunities. As this technology gains traction, understanding its mechanics, lifecycle, and applications becomes essential, especially for decision-makers steering financial organizations toward the future.

This guide breaks down the essentials of RWA tokenization, offers insights into the development lifecycle, and explores the growing need for an experienced RWA tokenization development company that can help financial institutions lead the next generation of banking.

Why is RWA Tokenization Non-Negotiable for Modern Banks?

The RWA Tokenization in the banking sector transforms static, illiquid assets into programmable, tradable, and divisible tokens that can be securely managed on decentralized platforms. It’s building resilient, transparent, and accessible financial infrastructure that aligns with global demands for efficiency, automation, and 24/7 financial service delivery. Here is how:

1. Lending and Credit Operations

Tokenization is redefining collateralized lending by introducing automation, transparency, and real-time asset verification. Banks can tokenize a range of real-world assets, such as real estate, invoices, or vehicle titles, to streamline credit issuance. Key benefits are:

- Automated underwriting via smart contracts that validate collateral in real-time.

- On-chain enforcement of lending terms and repayment schedules.

- Fraud reduction through immutable, auditable records on a permissioned blockchain.

2. Securitization and Capital Markets

In the capital markets space, RWA tokenization in banking is modernizing traditional securitization. Asset-backed securities (ABS)—including mortgage-backed securities and credit card receivables- can be tokenized and issued on blockchain platforms. The tokenization development services enable the investment banks to reach a broader spectrum of accredited investors while navigating fewer regulatory frictions. Key benefits include:

- Enhanced secondary market liquidity through fractional ownership.

- Direct investor participation, bypassing intermediaries like custodians or rating agencies.

- Lower issuance costs and faster settlement cycles.

3. Cross-Border Payments and Settlement

Cross-border banking transactions are traditionally slow and expensive due to multiple intermediaries, currency conversions, and reconciliation delays. When combined with ISO 20022-compliant protocols or integrated into existing SWIFT systems, tokenized payment rails maintain compliance while offering a major upgrade in transaction speed and cost-efficiency. Key outcomes include:

- Real-time settlement of international transfers.

- Reduced transaction fees by eliminating correspondent banking layers.

- Minimized reconciliation errors through shared ledger visibility.

4. Custody and Asset Management

As banks evolve into digital custodians, tokenized assets present a compelling opportunity to diversify services and increase client assets under management. By integrating RWA tokenization into wealth management and asset advisory models, banks can tap into new fee structures and attract digitally native investors. Key benefits include:

- Institutional-grade custody for tokenized equities, bonds, and alternative investments.

- Fractional investment products for retail or high-net-worth individuals.

- Automated dividend and yield distributions through smart contracts.

5. KYC/AML and Regulatory Compliance

Compliance remains a cornerstone of modern banking, and tokenization development services now enable smart contracts to embed compliance logic directly into digital asset lifecycles. Key benefits include:

- Automated Know Your Customer (KYC) and Anti-Money Laundering (AML) checks at the point of transaction.

- Seamless onboarding of new clients via blockchain-based digital identity.

- Ongoing compliance monitoring, reducing operational overhead, and audit costs.

Banks that adopt these capabilities gain a competitive edge in both customer experience and regulatory alignment, particularly as digital assets come under closer global scrutiny.

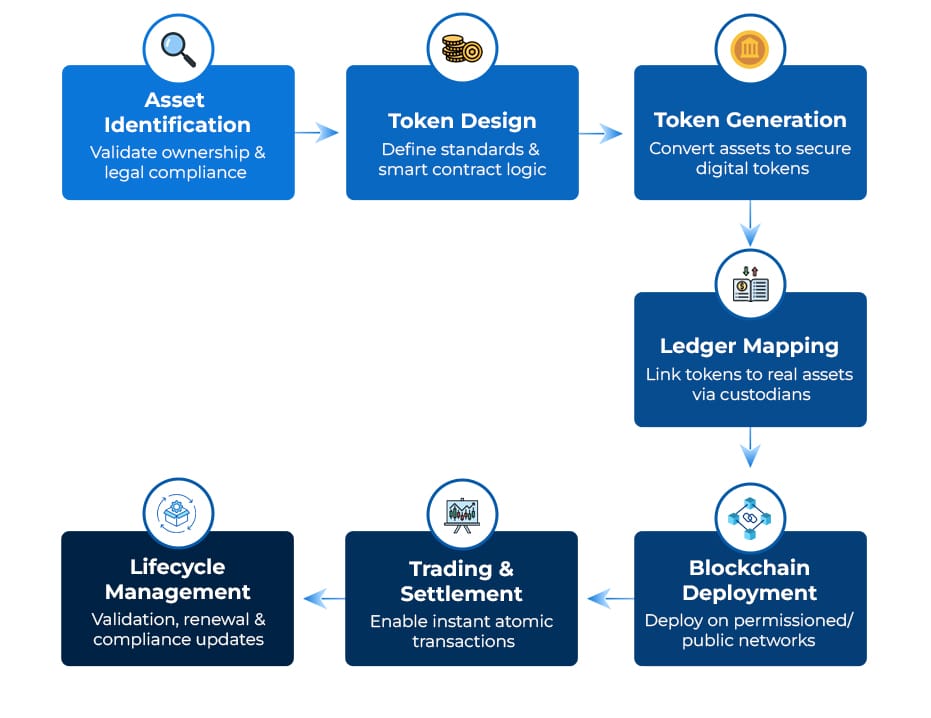

The RWA Tokenization Lifecycle in Banking

Successful RWA tokenization development requires a structured lifecycle that ensures data security, regulatory compliance, and long-term scalability. The RWA Tokenization Lifecycle in Banking typically involves the following stages:

1. Asset Identification and Due Diligence

Banks must start by identifying the real-world assets eligible for tokenization. This includes validating ownership, valuation, and legal compliance. Due diligence ensures the underlying asset is suitable for digital representation without regulatory or structural conflict.

2. Token Design and Framework Definition

Based on the asset class, developers create tokens that comply with international token standards (like ERC-1400 or ERC-20). Specifications such as divisibility, rights assignment, and smart contract logic are determined at this stage.

3. Token Generation

Using cryptographic methods, real assets are converted into secure digital tokens. These may represent full or fractional ownership, tailored to market needs.

4. Ledger Mapping and Custodianship

An internal ledger links each token to its corresponding real-world asset, supported by custodians or escrow agents. Banks often partner with third-party custodians for asset safekeeping and compliance management.

5. Deployment and Interoperability

Tokens are deployed on permissioned or permissionless blockchains, depending on the use case. For example, a regulated banking environment may favor permissioned DLT with access control mechanisms.

6. Trading, Settlements, and Secondary Markets

Banks can enable token trading on internal platforms or third-party marketplaces. Settlements become instantaneous (atomic), eliminating the need for complex clearing mechanisms.

7. Token Renewal and Lifecycle Management

To maintain security and compliance, tokens may undergo periodic validation, renewal, or even revocation. Banks must manage these lifecycle updates through secure vault operations.

Real-World Applications: Tokenization in Investment Banking

In investment banking, where data sensitivity, volume, and speed are paramount, tokenization delivers unmatched value. Confidential records, trades, and portfolios can be converted into tokenized formats for secure processing across systems.

Use Cases Include:

- Programmatic Trading: Investment banks are using tokenization to automate large-scale transactions while safeguarding sensitive data.

- Portfolio Management: Tokenized portfolios offer enhanced security and cross-border accessibility without compromising investor privacy.

- Data Governance: With token scope separation, different departments (e.g., compliance, trading desks) only access data relevant to their role.

These implementations are more than theoretical. Global banks like JPMorgan, Goldman Sachs, HSBC, BNY Mellon, and Deutsche Bank have already integrated tokenization into securities trading, supply chain finance, and digital custody platforms.

Key Technologies Behind Tokenization Platforms

Developing a secure, scalable RWA Tokenization Platform for Banking requires the integration of several technologies:

- Distributed Ledger Technology (DLT): The foundation for immutable record-keeping and smart contract execution.

- Smart Contracts: Automate and enforce rules around token transfers, dividend payments, or regulatory compliance.

- Oracles: Feed real-world data into blockchain systems (e.g., stock prices, interest rates).

- KYC/AML Modules: Ensure tokens are only issued to verified, compliant entities.

- Secure Custody Solutions: Protect real assets backing the tokens, whether physical (real estate) or financial (bonds).

When provided by a reputable RWA Tokenization Development Company, these components ensure regulatory adherence and system resilience from day one.

Takeaway

Tokenization represents a transformative moment for global banking, where operational efficiency, compliance, and digital innovation converge. From tokenization in investment banking to RWA tokenization lifecycle implementations, banks are seeing both technical and strategic value in partnering with specialized RWA Tokenization Development Companies and defining the future’s financial ecosystem.

Partner with Antier to Build Your Banking Tokenization Platform

Antier is a leading RWA tokenization development company helping banks embrace the future of digital finance. With robust tokenization development services, Antier builds secure, compliant, and scalable platforms tailored for real-world asset tokenization in banking. From smart contracts to regulatory integration, we simplify your tokenization journey. Empower your institution with innovative solutions designed for tomorrow’s financial ecosystem—partner with Antier to lead the transformation today.

Frequently Asked Questions

01. What is RWA tokenization and why is it important for modern banks?

RWA tokenization transforms static, illiquid assets into programmable, tradable, and divisible tokens, enabling banks to create a more resilient, transparent, and accessible financial infrastructure that meets global demands for efficiency and automation.

02. How does tokenization improve lending and credit operations in banks?

Tokenization enhances lending by automating underwriting through smart contracts, ensuring real-time asset verification, enforcing lending terms on-chain, and reducing fraud with immutable records on a permissioned blockchain.

03. What benefits does RWA tokenization bring to capital markets?

RWA tokenization modernizes securitization by increasing secondary market liquidity through fractional ownership, allowing direct investor participation, and reducing issuance costs and settlement times.