✨ AI Summary

- In the world of institutional finance, tokenized debt instruments are revolutionizing how capital markets operate.

- From BlackRock moving a $5.6B fund onto blockchain to Singapore's UOB launching a $50M digital bond, these innovative solutions are not just experiments but practical answers to real-world issues.

- By streamlining settlements, reducing fees, and enhancing liquidity, tokenized debt instruments offer faster access to capital and improved yields.

- This blog post delves into the workings of tokenized debt instruments, their benefits for institutions, and the various categories and applications available.

- Furthermore, it explores the key players in this evolving landscape and how to leverage these advancements for maximum impact.

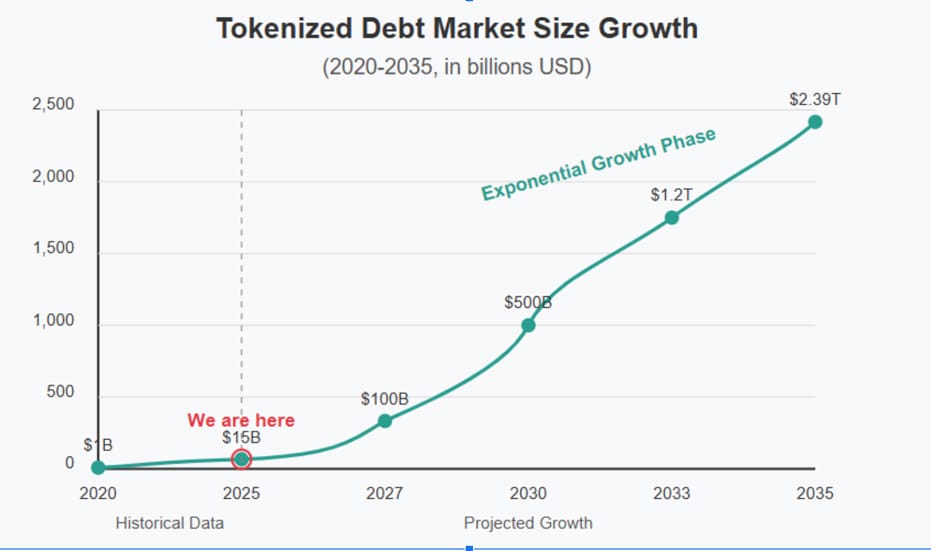

Tokenized debt instruments are changing how institutions access capital markets. BlackRock recently moved a $5.6B fund onto blockchain, while Singapore’s UOB launched a $50M digital bond, not as experiments, but as practical solutions to real problems.

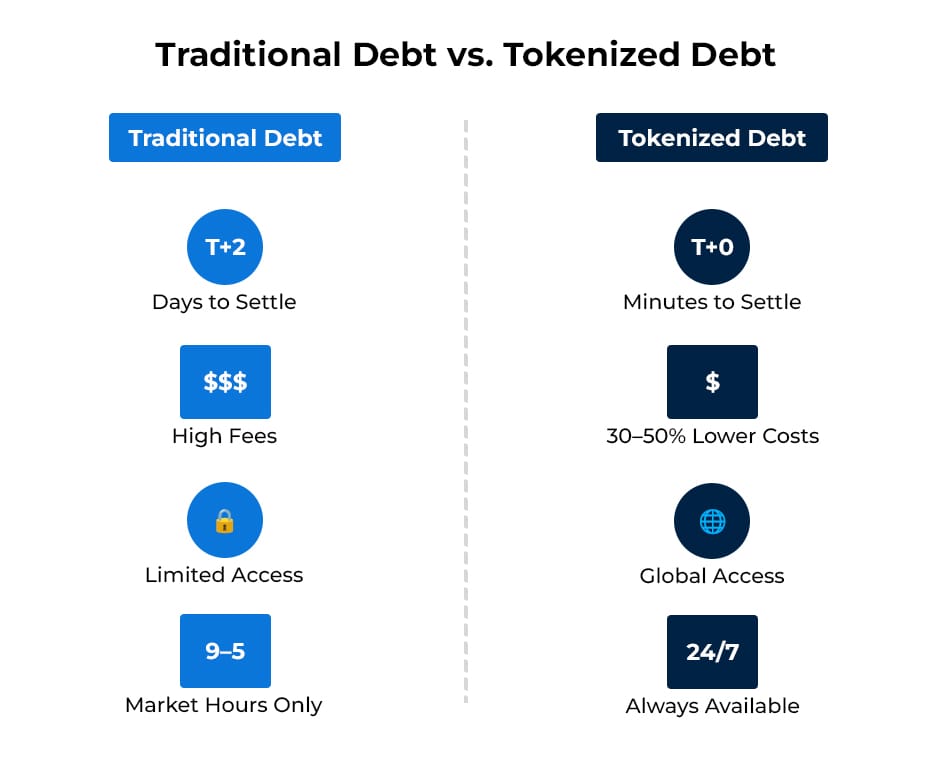

Tokenized Debt makes the settlements happen in minutes rather than days, fees drop substantially and yields consistently outperform traditional channels. It opens the gates to previously restricted debt markets with genuine 24/7 liquidity while smart contracts handle compliance automatically. This guide explores the Tokenized Debt instruments, how they work, who’s leading, and how to capitalize on them.

How Tokenized Debt Instruments Are Reshaping Institutional Finance?

Traditional debt markets suffer from significant inefficiencies, including slow settlement times, limited liquidity, and high intermediary costs. Blockchain-based asset-backed lending solves these problems by converting bonds, loans, and other debt instruments into digital tokens.

Key Benefits for Institutions:

- Lower Costs & Faster Settlement

Traditional bond issuance involves multiple intermediaries, including underwriters, custodians, and clearinghouses, each adding layers of fees to the process.

Tokenized debt instruments automate these processes via smart contracts, reducing issuance costs by 30-50% and cutting settlement times from days to minutes. This efficiency creates substantial savings for institutional borrowers and provides faster access to capital.

- Global Liquidity & Fractional Ownership

A corporate bond tokenized on-chain can be divided into smaller units, allowing mid-sized investors to participate in markets previously accessible only to large institutions.

Institutions gain access to a 24/7 secondary market instead of relying on over-the-counter desks with limited operating hours. This continuous market availability dramatically increases liquidity options for debt issuers.

- Regulatory-Compliant Transparency

Every transaction is recorded on an immutable ledger, simplifying audits and compliance reporting for regulatory bodies. This transparent record-keeping reduces the administrative burden while ensuring accountability.

Using RWAs as DeFi collateral ensures asset provenance while meeting Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements, creating a compliant framework that satisfies regulators.

- Data-Driven Risk Assessment

Traditional credit assessment relies on historical financial data and often overlooks real-time market conditions. On-chain debt instruments generate continuous performance data, allowing for more accurate risk pricing and dynamic yield adjustments.

Institutional lenders can access real-time loan performance metrics, enabling them to make more informed investment decisions and better manage their portfolios of tokenized assets.

- Programmable Compliance Features

Tokenized debt instruments can embed compliance requirements directly into the smart contracts governing their operation. These programmable features can automatically enforce investment restrictions, holding periods, and accreditation requirements.

This automation reduces compliance costs for institutions while providing greater certainty that regulatory requirements are consistently followed throughout the asset lifecycle.

Tokenized Debt Instruments: Key Categories and Applications

Tokenized debt instruments represent the digitization of traditional financial obligations through blockchain, enhancing tradability, accessibility, and operational efficiency. The primary variants include:

1. Tokenized Bonds: Digital Fixed-Income Securities

Tokenized bonds transform conventional debt securities into blockchain-based digital assets. These instruments maintain the fundamental characteristics of traditional bonds while introducing technological enhancements:

- Fractionalization: Enables division of bond denominations, permitting participation at lower investment thresholds.

- Continuous Trading: Facilitates secondary market transactions outside conventional trading hours.

- Borderless Access: Expands investor base beyond institutional participants to include global retail investors.

The tokenization process preserves bond attributes such as coupon payments and maturity dates while improving liquidity through blockchain’s inherent features.

2. Tokenized Loans: Distributed Lending Mechanisms

Tokenized loan structures revolutionize credit markets by enabling multiple lenders to participate in individual loan facilities:

- Pooled Funding: Converts loan obligations into digital tokens available for purchase by multiple creditors

- Risk Distribution: Allocates credit exposure across numerous investors rather than concentrating risk with a single institution

- Market Expansion: Provides capital access for borrowers who may not meet traditional lending criteria

This model has gained particular traction in decentralized finance (DeFi) ecosystems, where algorithmic protocols replace conventional intermediaries in loan origination and servicing.

3. Digital Promissory Notes: Programmable Debt Agreements

Digital promissory notes represent the blockchain-based evolution of traditional debt acknowledgment instruments:

- Automated Execution: Incorporates repayment terms into self-executing smart contracts

- Secondary Market Liquidity: Enables transferability of debt positions between parties

- Immutable Recordkeeping: Creates transparent, auditable transaction histories

These instruments bring standardization and efficiency to private credit markets that have historically operated with limited transparency.

Selection Criteria for Implementation

The appropriate tokenized debt instrument varies by use case:

- Long-term institutional debt: Tokenized bonds

- Collaborative lending models: Tokenized loans

- Short-term credit arrangements: Digital promissory notes

Who Needs a Tokenized Debt Platform?

1. Banks & Traditional Lenders

Problem: Bond issuance is slow, expensive, and restricted to large players.

Solution: By working with an RWA tokenization development company, banks can digitize syndicated loans and bonds, making them tradable on secondary markets. This transformation can reduce operational costs by up to 50% while expanding their investor base.

2. Asset Managers & Hedge Funds

Problem: Private credit is illiquid, locking capital for years with limited exit options.

Solution: Tokenizing private debt allows funds to offer early redemptions via decentralized exchanges. Fund managers can create more flexible investment products that still generate the stable yields their client’s demand.

3. DeFi Platforms Expanding to Institutions

Problem: Most DeFi lending relies on volatile crypto collateral, limiting institutional participation.

Solution: Integrating RWA collateral in DeFi (like tokenized corporate bonds) attracts institutional lenders seeking stable yields. These platforms can bridge the gap between traditional finance and the innovation of decentralized markets.

4. Governments & Municipalities

Problem: Municipal bonds have limited investor reach and outdated issuance processes.

Solution: Tokenizing sovereign debt opens funding to global retail and institutional investors. Governments can reduce their borrowing costs while creating more transparent fiscal management systems.

How Tokenized Debt Works: A Technical Deep Dive

1. The Tokenization Process

An RWA tokenization development company converts a real-world debt asset (like a bond or loan) into a digital token representing its value and rights.

Legal frameworks ensure the token represents enforceable ownership rights through trust structures, Special Purpose Vehicles (SPVs), or direct regulatory recognition. This legal foundation is essential for institutional adoption.

2. Smart Contracts for Automated Compliance

Interest payments, maturity dates, and default procedures are programmed into smart contracts that execute automatically when conditions are met.

For example, a tokenized corporate bond can automatically distribute coupon payments to all token holders on predetermined dates, eliminating the need for manual processing of interest payments.

3. Integration with DeFi Lending Protocols

Institutions can use tokenized debt instruments as collateral for loans in DeFi, unlocking additional liquidity without selling their assets.

Platforms like Centrifuge and Maple Finance already facilitate institutional borrowing with tokenized assets, creating new capital efficiency opportunities for traditional financial entities.

4. Regulatory Considerations

Most jurisdictions classify tokenized debt instruments as securities, requiring:

- KYC/AML checks for investors

- Licensed custody solutions for assets

- Compliance with local securities laws (SEC, MiCA, etc.)

- Tax reporting capabilities for investors

Building a Tokenized Debt Platform: Key Steps

1. Partner with an Experienced RWA Tokenization Development Company

Look for firms with expertise in:

- Blockchain infrastructure (Ethereum, Polygon, or private chains)

- Smart contract security audits and risk mitigation

- Regulatory compliance frameworks for multiple jurisdictions

- Integration capabilities with traditional financial systems

2. Define Your Asset Class & Investor Base

Will you tokenize corporate bonds, private credit, or sovereign debt? Each asset class has different legal and technical requirements.

Are you targeting institutional investors, accredited individuals, or retail participants? This decision affects your compliance approach and platform design.

3. Develop a Robust Compliance Layer

Embed identity verification (KYC) and accreditation checks directly into your platform’s onboarding process.

Ensure tax reporting automation for investors, simplifying their regulatory obligations and making your platform more attractive.

4. Ensure Liquidity & Secondary Market Support

Integrate with decentralized exchanges (Uniswap, Aave Arc) or create proprietary trading mechanisms for your tokenized assets.

Partner with market makers to ensure tight bid-ask spreads, creating confidence in the liquidity of your tokenized debt instruments.

5. Pilot with a Trusted Issuer

Start with a small-scale bond or loan issuance to demonstrate the effectiveness of your platform.

Gather feedback from institutional users before scaling to larger issuances or more complex debt structures.

The Future: Institutional DeFi Lending & Beyond

1. Growth of RWA-Backed Stablecoins

Institutions like JPMorgan are exploring deposit tokens collateralized by tokenized real-world assets, creating more stable digital currencies for institutional use.

These asset-backed stablecoins could become the backbone of institutional DeFi activity, providing the stability needed for widespread adoption.

2. Expansion into Emerging Debt Markets

Tokenizing emerging market bonds could unlock trillions in untapped liquidity. Real-World Asset Tokenization provides the transparency and risk management tools needed to make these markets more accessible.

This democratization of access could transform capital formation in developing economies while providing new yield opportunities for global investors.

3. AI-Optimized Risk Assessment

Machine learning models will assess credit risk for on-chain debt instruments in real-time, creating more accurate pricing models.

These systems will analyze platform data, market conditions, and issuer performance to provide dynamic risk assessments previously impossible in traditional debt markets.

Conclusion: The Time to Build Is Now

Institutional DeFi lending is gaining real momentum, with banks, asset managers, and even governments starting to explore tokenized debt. For those building in this space, it’s a rare chance to help redefine the future of global finance.

At Antier, we specialize in RWA tokenization and can help you tap into the growing market for tokenized debt. Let’s build a more open, transparent, and efficient financial world together.

Frequently Asked Questions

01. What are tokenized debt instruments and how do they benefit institutions?

Tokenized debt instruments are digital representations of bonds, loans, and other debt instruments on a blockchain. They benefit institutions by reducing issuance costs by 30-50%, cutting settlement times from days to minutes, and providing access to a 24/7 secondary market, enhancing liquidity and efficiency.

02. How do tokenized debt instruments improve liquidity for investors?

Tokenized debt instruments allow for fractional ownership, enabling mid-sized investors to participate in markets previously accessible only to large institutions. This creates a continuous market availability, significantly increasing liquidity options for debt issuers.

03. What role do smart contracts play in tokenized debt instruments?

Smart contracts automate processes involved in issuing and settling tokenized debt instruments, ensuring compliance and reducing administrative burdens. They facilitate faster transactions and enhance transparency by recording every transaction on an immutable ledger.