AI Summary

- Discover why over 40 million individuals are turning to crypto wallets as their preferred financial interface, challenging traditional banking norms.

- In a shift towards decentralized control and transparency, crypto wallets offer users true self-custody, layered security, real-time auditability, yield-generating features, multi-chain asset management, transparent fee models, and regulatory alignment.

- This milestone signifies a paradigm shift towards mainstream financial utility, with top reasons including ownership, security, auditability, yield generation, asset management, fee transparency, and regulatory compliance.

- As users seek resilient, borderless, and verifiable financial systems, crypto wallets are emerging as the new global standard for digital asset custody.

- Explore how these solutions redefine the way value is stored, transacted, and secured worldwide, offering a dynamic and secure alternative to traditional banking.

Have you ever questioned why millions are rethinking their relationship with traditional banks in today’s hyper-digital financial landscape? Across the globe, financial institutions are being challenged by inefficiencies, cross-border restrictions, and growing mistrust fueled by centralized control and high-profile failures.

In response, over 40 million people have quietly shifted to crypto wallets—not just for trading, but as their go-to financial interface. Crypto wallet development solutions are not just digital accessories; they represent a re-architecture of trust, ownership, and control. While banks continue to operate on closed, permissioned infrastructures, crypto wallets empower users with real-time access, transparent records, and programmable security, powered by the principles of decentralization. The transition isn’t accidental; it’s a reflection of how users are seeking systems that are resilient, borderless, and verifiable by design.

Scroll through the blog to explore why users trust crypto wallets like bank accounts!

Market Momentum: Why the 40M+ Crypto Wallet Adoption Milestone Matters?

Surpassing 40 million active users marks a paradigm shift from niche experimentation to mainstream financial utility. Top cryptocurrency wallet service providers like Bitget have doubled their user base in six months, outpacing many centralized exchanges and underscoring the demand for non-custodial, programmable finance.

Regional adoption is equally telling: Chainalysis’ 2024 Global Crypto Adoption Index ranks Central and Southern Asia and Oceania as the fastest-growing markets, where underbanked populations are leapfrogging legacy banking via self-sovereign wallets. This convergence of rapid user growth, technological maturity, and geographic breadth validates crypto wallet development solutions as the new global standard for digital asset custody. The million milestone thus signifies not just growth in numbers but the crystallization of wallets as fundamental Web3 infrastructure, poised to redefine how value is stored, transacted, and secured worldwide. Let us begin to understand the key reasons.

Top Reasons: Why People Trust Crypto Wallet Development Solutions Just Like Bank Accounts?

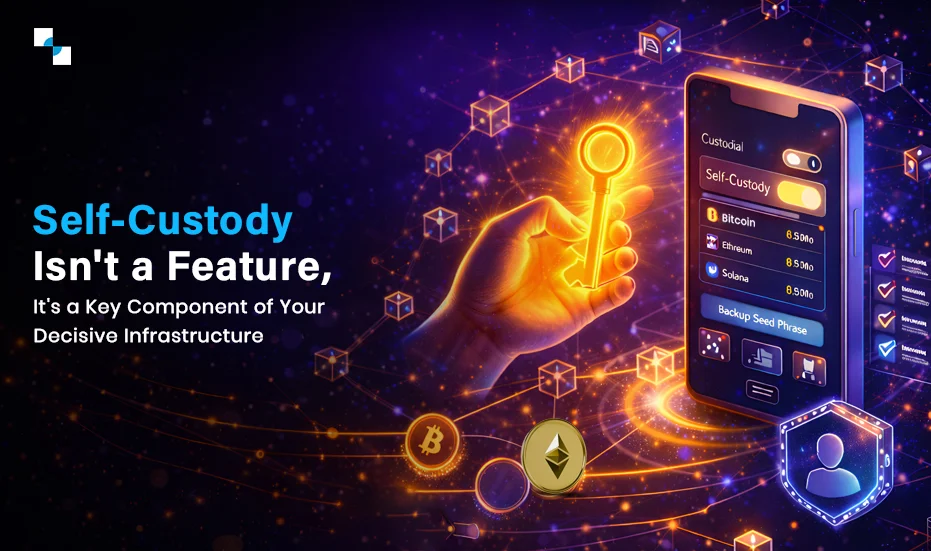

Reason 1. True Self-Custody & Zero Counterparty Risk

By storing private keys locally—either in a secure mobile app or hardware device—users assume full ownership and responsibility for their assets. This non-custodial wallet development model eradicates exposure to third-party insolvency, platform freezes, or unilateral fund freezes. Seed phrases, encrypted and backed up offline, enable seamless wallet recovery without needing KYC gatekeepers or customer support processes. This direct control resonates with individuals who value sovereignty over their finances, providing confidence equivalent to having a personal vault secured by military-grade encryption.

Example : A user installs a non-custodial wallet, writes down their seed phrase offline, and transfers 1 ETH in. With sole access to the private keys—no exchange involved—they know their funds cannot be frozen or seized and can be recovered on any device.

Reason 2. Institutional-Grade Layered Security

Modern cryptocurrency wallet development solutions integrate multi-signature schemes, threshold cryptography (MPC), and hardware-secure enclaves (HSMs/TEEs) to fragment and protect key material. Transactions require multiple independent approvals, mitigating single-point-of-failure risks. Providers undergo SOC 2 and ISO 27001 audits, ensuring processes align with bank-grade security standards. This layered architecture, combining on-device biometric locks with off-chain key-share distribution, defends against both remote exploits and insider threats. Users benefit from institutional assurances without sacrificing the agility and transparency of Web3.

Example : When initiating a large transfer, the crypto wallet splits the signing request across three servers using MPC; the user confirms via biometric unlock on their phone. Only after all parties sign does the transaction proceed, mirroring a bank’s multi-authority approval process.

Reason 3. Immutable, Real-Time Auditability

Every transaction—whether a deposit, swap, or contract call—is recorded on a public blockchain, timestamped, and cryptographically hashed. Users can inspect their entire history instantly through their cryptocurrency wallet app development solutions by viewing analytics dashboards and exporting verifiable proofs for accounting or compliance. Unlike monthly bank statements, this on-chain ledger provides sub-second visibility into funds’ movements and gas costs. The transparency fosters trust, since no off-book adjustments or hidden reserves can exist. Institutions leverage these immutable records to underpin AML/CTF programs and reconcile portfolios in real time.

Example : After swapping USDC for DAI, the user opens a blockchain explorer and instantly sees the transaction hash, timestamp, and token amounts. They export the entry as a CSV proof, reconciling it directly against their budgeting software without waiting for monthly statements.

Reason 4. Native Yield-Generating Features

Crypto wallet app development solutions embed DeFi protocols—staking pools, lending markets, and liquidity-mining vaults—so users can deploy idle assets for passive income. Annualized yields of 5–15 percent become accessible through a single interface, automatically compounding rewards on-chain. Users no longer toggle between separate platforms; everything from deposit to reward distribution occurs within the wallet. This integration redefines the concept of a “savings account,” offering returns that outpace traditional banks and turning wallets into dynamic financial hubs rather than static storage tools.

Example : A user stakes 2 ETH directly within their wallet’s DeFi widget into a liquid staking protocol. Rewards accrue in real time, showing a growing stETH balance. Without leaving the wallet, they reinvest earned tokens back into the pool to maximize compound yield.

Reason 5. Seamless Multi‑Chain Asset Management

An All-In-One Shop cryptocurrency wallet now consolidates assets across Ethereum, Solana, BNB Chain, Avalanche, and more, using built-in bridges and cross-chain messaging. Users view and manage all tokens in a unified portfolio, eliminating the need for multiple addresses or apps. Cross-chain transfers occur behind the scenes via secure relayers, with final confirmations back to the same UI. This interoperability ensures that liquidity and opportunities—whether NFTs, stablecoins, or DeFi positions—are accessible without technical friction or siloed custody, mirroring the convenience of a multi-currency bank account.

Example : Holding USDT on Ethereum and BNB Chain, a user selects “Bridge” in their wallet and moves 1,000 USDT to BNB Chain. Ten minutes later, the unified balance updates under the same address—no additional logins or separate apps required.

Reason 6. Transparent, Predictable Fee Models

EIP‑1559 and fee estimation tools show users the exact base fee, priority fee, and total gas cost before signing. There are no hidden maintenance or service charges: every fee burns on-chain or goes to validators. Users choose speed vs. cost trade-offs with full visibility, akin to seeing exact wire transfer fees in advance. This clarity contrasts with opaque bank charges, where maintenance, overdraft, or foreign-exchange fees often surprise customers after the fact.

Example : Before sending 0.3 ETH, the user views the fee breakdown—0.001 ETH base fee and 2 gwei priority fee. Confident there are no extra charges, they approve the transaction, knowing exactly how much value will arrive in the recipient’s address.

Reason 7. Regulatory Alignment & Institutional Backing

Top cryptocurrency wallet development companies now embed zero-knowledge KYC modules (e.g., zk-KYC) in their wallet platforms and partner with insured custody networks. They operate within global sandbox frameworks—UAE, Singapore, and the UK—demonstrating compliance with AML/CTF and Travel Rule requirements. Smart-contract whitelists enforce regulatory parameters on-chain without compromising privacy. These measures deliver the legal assurances, insurance protections, and audit capabilities that traditional banks provide, reassuring both retail users and institutional clients that their wallet balances enjoy the same governance safeguards.

Example : When accessing a token sale, the user completes a zk-KYC check within the crypto wallet platform , receiving an on-chain credential. The sales contract verifies this credential, permitting participation. Behind the scenes, insurers underwrite custody, ensuring funds are covered against platform risk.

Hire Certified Experts for a 100% Successful Crypto Wallet Launch!

Are you planning to launch something impactful in this highly competitive market? Connect with a leading cryptocurrency wallet development company. Antier specializes in delivering fully white-label crypto wallet platforms that are DeFi-enabled and market-ready in just 2–3 weeks. Our turnkey solution includes multi-chain support, smart-contract-based account abstraction, integrated fiat on-ramps, and intuitive UI/UX, all customizable to your brand. We handle deployment, token integrations, and ongoing maintenance so you can focus on customer growth. Launch swiftly with our expert team guiding you through every step—from architecture design to live launch—ensuring a robust, compliant crypto wallet ecosystem that captures market demand from day one. Partner with us today!

Frequently Asked Questions

01. Why are people moving away from traditional banks to crypto wallets?

People are shifting to crypto wallets due to inefficiencies, cross-border restrictions, and growing mistrust in traditional banks, seeking systems that offer real-time access, transparency, and decentralization.

02. What does the adoption of over 40 million crypto wallets signify?

The adoption of over 40 million crypto wallets marks a shift from niche experimentation to mainstream financial utility, indicating a demand for non-custodial, programmable finance solutions.

03. What are the key benefits of using crypto wallets compared to traditional bank accounts?

Key benefits of crypto wallets include true self-custody, zero counterparty risk, and full ownership of assets, allowing users to store private keys securely and maintain control over their financial resources.

{kind=link}