AI Summary

- SBI VC has launched Japan's first licensed USDC lending service at a high APY of 10%, significantly outperforming traditional USD deposits.

- This move marks a shift towards full-service crypto banking hubs, with users now comparing APYs like they once compared trading fees.

- The broader crypto lending landscape is booming, with CeFi+DeFi lending hitting new highs.

- Exchanges are evolving into yield-driven ecosystems, integrating lending to enhance user retention and revenue beyond trading fees.

- The integration of lending not only boosts liquidity but also positions exchanges as yield-first platforms in a competitive market.

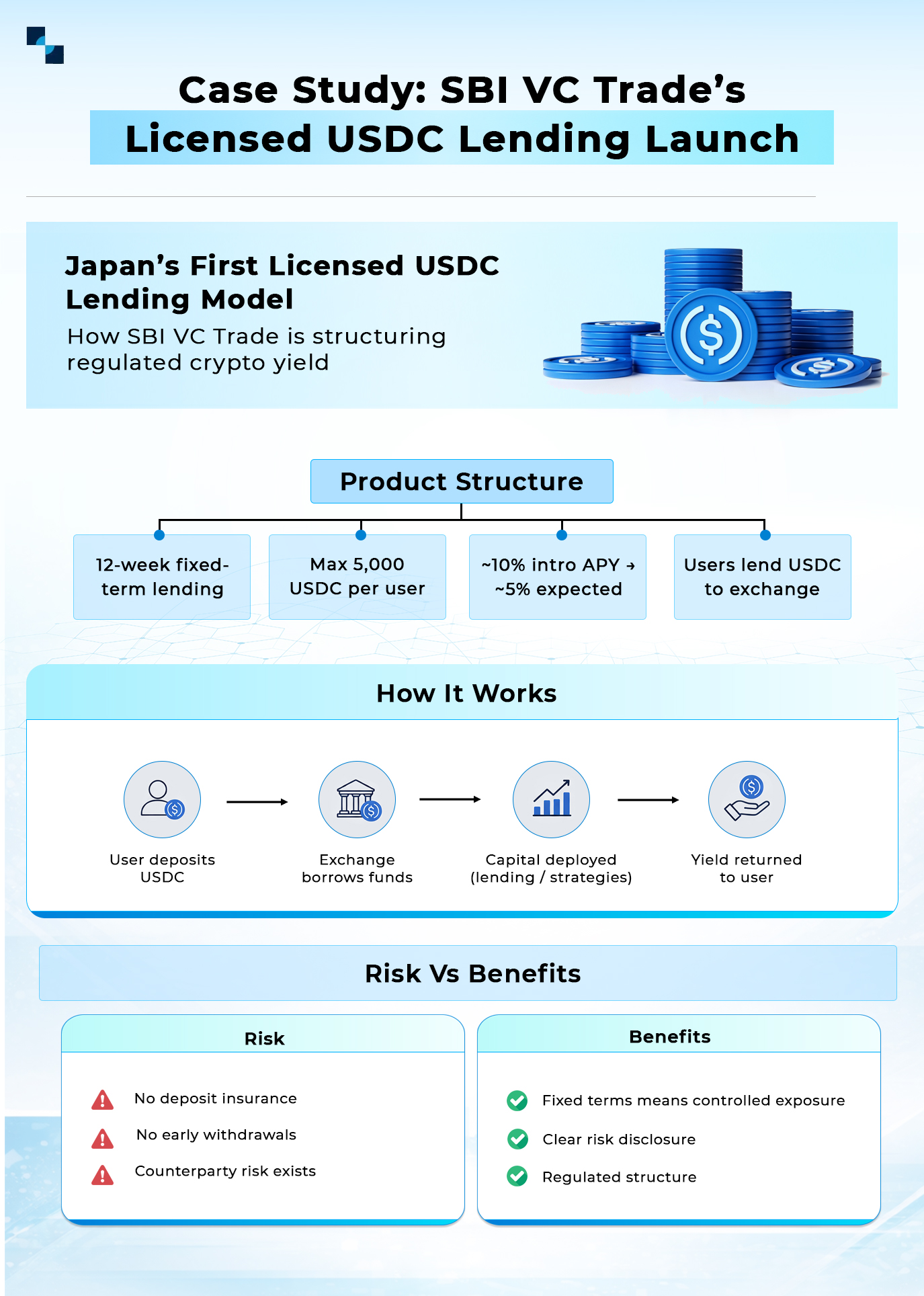

SBI VC launches Japan’s first-ever licensed USDC lending service at 10% APY, dwarfing traditional USD deposits offering 0.1-4% yield. This isn’t just another watershed moment for the investors but for exchanges too since they are transforming into full-service crypto banking hubs. The March 19, 2026 rollout offers retail investors a 12-week fixed-term product capped at 5,000 USDC per user, allowing customers to lend their USDC to exchange, which uses them to generate yield. These yield-driven, user-friendly and risk-labelled products position VASPs in direct competition with tradFi providers.

The broader crypto lending landscape is skyrocketing with crypto-collateralized lending (CeFi+DeFi) reaching a new ATH of $73.59B at the end of Q3 2025, up from 38.5% QoQ. CeFi lending alone reached $24.37 billion in Q3 2025, underscoring how fast licensed platforms are capturing capital from users who now compare APYs the way they once compared trading fees.

For founders, operators and white label exchange builders, this moment is both a warning and an opportunity. In markets like Japan, users are starting to compare crypto lending yields from platforms like SBI VC Trade with returns from traditional banks, turning CeFi lending into a practical alternative to bank deposits.

As lending attracts liquidity and keeps users engaged, capital is shifting from spot-only exchanges, the key question for founders is: how can new platforms integrate safe, compliant lending from day one?

The Shift From Simple Trading To Yield-Driven Exchange Ecosystems

Users no longer judge exchanges solely on spreads and liquidity. APYs are the new battleground. As more users prioritize yield generation, exchanges are evolving into single, sticky ecosystems that combine staking, lending, yield vaults, social feeds, and other engagement layers.

Spot-only exchanges offer little incentive for users to park their capital long-term, which erodes user stickiness. In contrast, platforms integrating lending, and staking see higher capital retention as users prefer locking their assets to earn yield instead of arbitraging quickly and leaving. This stickiness feeds deeper liquidity across spot, margin, and derivatives, creating a self-reinforcing liquidity flywheel.

directly feeds deeper liquidity across spot, margin, and derivatives, creating a self-reinforcing liquidity flywheel.

That’s why white label cryptocurrency exchanges with built-in lending modules are essential for anyone seeking to launch their crypto trading platform. These integrated lending layers are becoming the new liquidity engine and retention moat for modern exchanges.

Why is Integrated Lending Now a Strategic Requirement For Global Exchanges?

- Increased User Retention

The spot-only exchanges depend on trading activity for retaining their users. Lending integration turns it into a multi-product engagement approach. The retention is then built into the product since capital gets locked.

- Revenue Moves Beyond Trading Fees

Spot fees are compressing globally. Crypto exchanges have to come up with better revenue engines. Integrated lending introduces interest spreads, borrowing demand monetization, and liquidity-driven revenue. This creates non-cyclical revenue streams, even in low-volume markets.

- Liquidity Becomes Programmatic

Instead of relying only on traders for the liquidity, the lending-integrated crypto exchange software activates the idle assets, bringing in internally generated liquidity.

- Yield-as-a-Service Exchanges

The competitive benchmark is shifting from best trading experience to best capital efficiency platform. This necessitates the crypto lending module integration in exchanges.

How Antier’s White Label Crypto Exchange Supports Integrated Lending

Antier acts as the infrastructure layer for teams that want to launch lending-enabled exchanges without building everything from scratch.

Core Capabilities of Lending-Integrated White Label Cryptocurrency Exchange

| Feature | Benefit for Exchange Operators |

| Plug-and-play lending & borrowing module | Faster launch of lending products similar to SBI’s model |

| Smart contract-based escrow & collateral management | Transparent, over-collateralized lending with controlled risk |

| Compliance-ready modules (KYC/AML, admin controls) | Easier adaptation to local regulations (MiCA, Japan, GCC, etc.) |

| Fiat-to-crypto rails + BaaS integrations | Enables a “crypto banking” experience beyond trading |

Crypto Exchanges as Yield-First Platforms

The global crypto lending platform market, valued at $10.68 billion in 2025, is projected to grow by 18.8% CAGR and reach $25.06 billion by 2030. Cryptocurrency exchange software solutions are not leaving this opportunity and so are becoming yield-centric financial platforms.

What’s Coming Next

- Custom lending strategies (retail + institutional tiers)

- Integrated staking, vaults, and structured products

- Dynamic risk engines tied to market conditions

At the same time regulators will demand stricter disclosure and lending products will face closer scrutiny. This means winners will be the platforms that treat yield as a core feature, build compliance into product design and adapt quickly to regulatory changes.

Cryptocurrency exchange software infrastructure providers like Antier enable that flexibility without sacrificing speed. This ensures exchanges can scale lending capabilities without compromising on risk management or compliance.

Connect with our experts to explore custom exchange development and lending-enabled white-label solutions.

Frequently Asked Questions

01. What is SBI VC's new USDC lending service and what are its key features?

SBI VC has launched Japan's first licensed USDC lending service offering a 10% APY, significantly higher than traditional USD deposits. The service, rolling out on March 19, 2026, allows retail investors to lend up to 5,000 USDC for a 12-week fixed term.

02. How does the crypto lending landscape compare to traditional banking?

The crypto lending landscape is rapidly growing, with crypto-collateralized lending reaching an all-time high of $73.59 billion by the end of Q3 2025. Users are increasingly comparing yields from crypto lending platforms like SBI VC Trade to traditional bank returns, making CeFi lending a viable alternative.

03. Why are exchanges evolving into yield-driven ecosystems?

Exchanges are shifting from simple trading to yield-driven ecosystems because users now prioritize yield generation over just trading fees. By integrating lending and staking, these platforms enhance user engagement and capital retention, creating deeper liquidity across various trading options.